Trust income allocations can seem complicated for Canadian beneficiaries and trustees. However, like other tax slips in Canada, T3 slips serve a simple purpose – to report any income earned in a trust that gets allocated to beneficiaries.

With some key facts about what T3 slips are, who needs to file them, and how to report T3 income properly, you can ensure full compliance with Canada Revenue Agency requirements.

What is a T3 Slip?

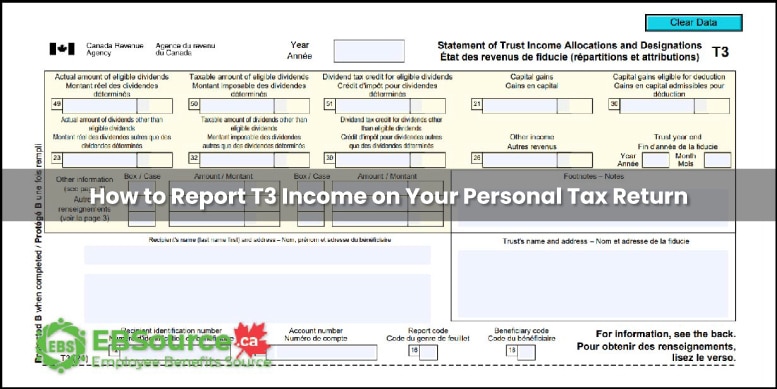

A T3 slip, formally known as the Statement of Trust Income Allocations and Designations, is a tax information slip that reports income earned in a trust that is allocated to beneficiaries.

In Canada, trusts are considered separate legal entities and must file a T3 trust tax return annually. As part of this filing, trusts are required to distribute T3 slips to any beneficiaries who receive allocations of income earned within the trust.

The T3 slip outlines the types and amounts of income allocated to the beneficiary for tax reporting purposes. The four most common types of income shown on a T3 slip are:

- Interest: This includes interest earned by the trust through investments like bonds, GICs, mortgages, bank accounts, or loans.

- Dividends: Earnings the trust received through dividends issued by corporations on stocks held within the trust’s investment portfolio.

- Capital gains: These apply when the trust sells assets like stocks, bonds, real estate, or other investments at a profit.

- Foreign business income: Profits allocated to the beneficiary from a business owned and operated by the trust in a foreign country.

That said, T3 slips help beneficiaries report and pay tax on the trust income they receive by giving them the information needed for their personal tax return.

When Do You Receive a T3 Slip?

T3 slips are issued to report income allocations for the trust’s relevant tax year. This means that as a beneficiary, you can expect to receive a T3 slip within 90 days after the end of the tax year of the trust.

For example:

- A trust with a December 31 year-end must issue T3 slips by March 31.

- One with a June 30 tax year-end has until September 30 to provide T3 slips.

The slip provides details on the types and amounts of income you received from the trust in that tax year. This allows you to report the income accurately on your personal tax return.

How Should a Trust File Its T3 Return and Slips?

When a trust reaches its tax filing deadline, filing a complete T3 return along with T3 slips for beneficiaries involves five key steps:

- Determine total income and allocations: Collect all income and distribution details to calculate totals for the T3 return.

- Prepare T3 slips for each beneficiary: Include their name, SIN, income type, and amounts allocated.

- File T3 return and slips with CRA: File by mail or electronically through My Trust Account within 90 days of year-end.

- Distribute T3 slips to beneficiaries: Ensure each receives their individual T3 slip by the deadline.

- Correct any errors: File an amended return and redistribute slips if any mistakes are found.

Meeting the filing deadline avoids potential penalties from the CRA and ensures beneficiaries have their T3 slips in time to file their personal tax returns accurately.

How to Report T3 Income on Your Personal Tax Return

With your T3 slip in hand, how do you properly report the amounts in your own tax return to the Canada Revenue Agency? Find out more in the sections below.

Where to Report Each Type of T3 Income

The T3 slip contains boxes with specific income types and amounts allocated to you as the beneficiary. Each amount must get transcribed carefully onto the corresponding line or schedule when you file your own personal tax return.

| T3 Slip Box | Income Type | Where to Report on Personal Return |

|---|---|---|

| Box 13 | Interest income | Enter on Line 121 as regular interest income |

| Box 14 | Dividend income | Report on Line 120 as taxable dividends |

| Box 15 | Capital gains | Enter taxable amount on Schedule 3 |

| Box 16 | Foreign business income | Report as self-employment income on Form T2125 |

Failure to properly transcribe T3 amounts risks audits or reassessments for incorrectly reporting income.

Adjusting Marginal Tax Brackets

In addition to reporting T3 income accurately, you must consider how the additional income affects your total income and marginal tax bracket for the year.

Even small amounts of additional interest or dividends could push your income into a higher bracket. Ensuring the proper marginal rate applies to each type of T3 income is critical.

Implications for Tax Credits and Deductions

With the extra income from a T3 slip, also consider how eligibility for certain credits or deductions may change.

For example, adding the T3 income could:

- Reduce your Canada Child Benefit if total family income exceeds thresholds

- Decrease your Age Credit claim if net income is now too high

- Limit the ability to claim the spouse credit based on new total income amounts

To avoid reassessments, ensure all calculations reflect the T3 amounts where applicable. Thoroughly review which income-tested credits and deductions may be affected.

Deadlines to Report T3 Income

You should integrate T3 amounts when filing your personal tax return for the year. Common deadlines for personal returns are:

- April 30 for most individuals

- June 15 if self-employed

- December 31 at the latest if the spouse or partner is self-employed

File by the deadline to avoid late filing penalties. The standard CRA penalty is 5% of any unpaid tax owing, plus 1% compounding each month the return is late.

Why Did I Get a T3 With No Income Received?

Sometimes, T3 slips can be puzzling, especially when they show the income you never directly received. This often happens with mutual fund trusts.

The reason is that mutual fund trusts must allocate their income earned to investors according to the number of shares they hold. Even if distributions are reinvested, the income itself is still taxable.

For example, say a mutual fund earned $100,000 of interest and capital gains in 2022. An investor who owned 5% of the fund on distribution day would receive a T3 for 2022, reporting $5,000 of income, even if they chose to reinvest the distribution.

So don’t be alarmed if your T3 shows income you didn’t actually collect. It’s simply your share of what the trust itself earned that year.

What Penalties Apply for Late or Incorrect T3 Filing?

To encourage full compliance, CRA applies penalties for late filing or mistakes on T3 returns:

- Late filing penalty: This applies if a T3 return with amounts owing is filed past the deadline. Depending on the number of days late and the amounts owing, the penalty can range from $100 to $7,500.

- $25 daily late filing fee: Even with no taxes owing, a penalty of $25 per day (minimum $100) applies for T3 returns filed after the deadline.

- Incorrect reporting penalties: If errors in income allocations or deductions are found, penalties ranging from 20% to 100% of the incorrect amount may apply, depending on the severity.

How Can You Correct Mistakes or Handle Lost T3 Slips?

Sometimes, trustees may need to revise T3 slips that were already issued to beneficiaries. There are specific procedures to follow depending on the situation:

Amending T3 Slips

If you notice an error on an existing T3 slip, you must prepare an amended T3 slip to correct the information. Clearly mark “AMENDED” on the new slip and fill out all boxes, including data that was correct on the original. Provide two copies to the beneficiary and file one copy with the CRA explaining the amendment reason.

Cancelling T3 Slips

To cancel a T3 slip that should not have been issued, prepare a new slip without changing any original details. Mark the new slip as “CANCELLED” and submit it to the CRA. This ensures the slip gets nullified and any related amounts are not reported.

Adding T3 Slips

If you missed sending certain T3 slips originally, file any additional slips separately, marked “ADDITIONAL.” Do not file another T3 Summary. Provide copies to each new recipient. Filing additional slips late can risk penalties.

Replacing Lost T3 Slips

If a beneficiary loses their T3 slip, issue a replacement marked “DUPLICATE,” but do not send copies to the CRA. Keep records of replaced slips. The beneficiary can still report the income without the physical slip.

How is a T3 Slip Different from a T4, T4A or T5 Slip?

T3 slips serve a distinct purpose from other common Canadian tax slips like the T4, T4A, and T5:

Let’s see how the table below summarizes the key differences:

| Tax Slip | Issuer | Income Type | Recipient |

|---|---|---|---|

| T3 | Trusts | Allocated trust income like capital gains, interest, and foreign business income | Trust beneficiaries |

| T4 | Employers | Employment income like salary and benefits | Employees |

| T4A | Pension funds, scholarships, etc. | Pensions, annuities, RESPs, other | Pensioners, students |

| T5 | Banks, investment firms | Interest, dividends, royalties | Investors |

Key Takeaways on T3 Slips

Here’s a quick summary of the most important things to know about T3 slips.

- T3 slips report any income from a trust allocated to beneficiaries for tax purposes.

- Almost all trusts must issue T3 slips to beneficiaries within 90 days after year-end.

- As a beneficiary, report T3 income on the appropriate lines and schedules when filing your personal tax return.

- Review T3 slips carefully and include the income reported, even if you didn’t directly receive an actual distribution.

- Late filing and mistakes on T3 returns can lead to significant financial penalties from CRA.

Understanding the purpose of T3 slips takes the confusion out of reporting trust income. With our guidance on where and how to report T3 amounts, both trustees and beneficiaries can file accurately and avoid issues with CRA. At the end of the day, proper trust income reporting means more dollars in your pocket and less stress at tax time.

FAQs about T3 Slips

When do I receive my T3 slip?

Trusts must issue T3 slips to beneficiaries within 90 days after their tax year end. For a December 31 year end, you'll receive it by March 31.

How do I report T3 income on my tax return?

Each type of income on the T3 gets entered on a specific line of your personal tax return. Interest on Line 121, dividends on Line 120, capital gains on Schedule 3.

Why did I receive a T3 slip with no income distributed?

Mutual fund trusts allocate income to investors based on units held, even if distributions were reinvested. You must still report allocated income on a T3 slip.

Where do I mail my T3 trust return?

Trustees must send paper T3 returns to the specific CRA tax centre noted on the forms. Electronic filing through My Trust Account is also available.

How long should I keep my T3 slips?

Keep T3 slips for a minimum of 6 years in case CRA reviews your tax returns. The standard reassessment period for individuals is 3 years plus an extra 3 years.

How is a T3 slip different from a T5?

A T3 reports allocated trust income while a T5 reports investment income like dividends and interest directly to the recipient. They serve different purposes.